The mortgage-delinquency rate among so-called subprime borrowers reached 25% in the first quarter but appears to be leveling off, rising only slightly in the second quarter. The pace of delinquencies for prime borrowers is accelerating. Since prime loans account for 80% of U.S. bank exposure to mortgages and credit cards, these losses could ultimately exceed those from weaker borrowers.

"The subprime pain is in the rearview mirror," says Sanjiv Das, head of Citigroup Inc.'s mortgage business, which is seeing delinquencies rise among prime borrowers, who make up three-quarters of its mortgage portfolio.

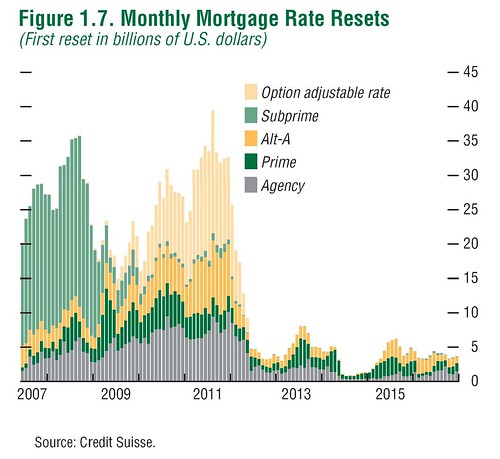

Well, I suppose we can finally state that "Subprime is contained". Actually there's a reason the defaults for subprime are dropping off, that's because the interest rate resets are mostly done so the defaults which lag the resets by a few months have been tapering off over the summer and should continue to fall off into next year. See the Credit Suisse

mortgage reset chart, subprime is mostly behind us.

The bad news is Alt-A and Option ARMs are still ahead of us, we're just about to get into the juicy part of the next mortgage interest reset cycle which will set off a whole new wave of defaults. The really bad news is this:

Bloomberg link

Excerpt:

The percentage of loans on which foreclosure actions were started was 1.36 percent, down from 1.37 percent in the first quarter, driven by the decline in subprime loans. New foreclosures on prime loans increased to 1.01 percent from 0.94 percent, while subprime loans dropped to 4.13 percent from 4.65 percent, Brinkmann said.

The delinquency rate for prime loans rose to 6.41 percent from 6.06 percent, and the share of prime loans in foreclosure increased to 3 percent from 2.49 percent.

And this

Housingwire link

Excerpt:

A slower cure rate among delinquent loans erased improvements in the number of loans rolling into delinquency status among US residential mortgage-backed securities (RMBS), according to Fitch Ratings.

Cure rates decrease as fewer delinquent loans return to current payment status each months. The prime cure rate slipped from an average 45% during ‘00-’06 to 6.6% today. Alt-A cure rates dropped to 4.3% from an average 30.2% and subprime cure rates fell to 5.% from an average 19.4%.

“Recent stability of loans becoming delinquent do not take into account the drastic decrease in delinquency cure rates experienced in the prime sector since the peak of the housing market,” said managing director Roelof Slump in a corporate statement.

“Whereas prime had previously been distinct for its relatively high level of delinquency recoveries,” Slump added, “by this measure prime is no longer significantly outperforming other sectors.”

While prime loans are still going delinquent & defaulting at a much lower rate than subprime, the pool of prime loans is much larger so even a relative low rate of defaults results in tons of foreclosures. The most worrying part is the "cure rate", which is the percentage of loans which get back on track & up to date after a missed payment. For prime to drop from 45% to only 6.6% is very bad, it means once a payment is missed the home is almost certainly headed for default & foreclosure. Prime mortgages have never behaved this way, at least not since the last depression. When the resets start in earnest we'll be in for some interesting times. Another mortgage crisis is pretty much guaranteed.

{kind=link}