Its a bit after one, so the numbers SEEM to make sense, but if they do... what the hell?"Lenders appear to be on track to initiate 2.25 million foreclosures this year, up from an average annual pace of less than 1 million during the pre-crisis period"

Okay, if something around one million is not a "crisis" but business as usual, what exactly is going on with the multi trillion bailouts?

At the peak, the median price of homes was running around $225K. If 1.25 million more than normal of those defaulted, the total amount financed, assuming zero down, would be roughly $280 billion.

Okay, now let's add a huge margin of error and assume the homes in default were valued at three times the median price, or $675K, and the total amount financed was $840 billion.

On average, housing prices across the country are down around 20%. Again, allowing a big margin of error, let's assume all of the foreclosures took place in the hardest hit markets and the drop in value was 40%, instead of 20%.

That would put the losses on those loans at $336 billion. If we assume the housing market was at peak two years ago, the total losses for the past peak period would be at twice that amount, or $672 billion. That number is likely a very high estimate.

Now, let's go back and recalculate based on the median and average. The total loan loses for the two year period would be $112 billion. That number is likely a very low estimate.

If you split the difference, the losses would be a little under $400 billion, which I don't think would be all that bad of a ballpark estimate.

So, here's the anomaly.... $400 billion, in actual loan losses from the bursting housing bubble, is less than 1/20th of the $8.5 trillion in taxpayer funded bailout money.

Where did/does the other $8.1 trillion go?

For about half the headlined $700 billion bailout, every single loan on a foreclosed home this year could have been purchased and refinanced at the current market value, with the money going toward writing off the difference.

Where DID all our money go?

This one needs an economist or an accountant

Moderators: Alyrium Denryle, Edi, K. A. Pital

-

CaptainChewbacca

- Browncoat Wookiee

- Posts: 15746

- Joined: 2003-05-06 02:36am

- Location: Deep beneath Boatmurdered.

This one needs an economist or an accountant

Link

Stuart: The only problem is, I'm losing track of which universe I'm in.

You kinda look like Jesus. With a lightsaber.- Peregrin Toker

You kinda look like Jesus. With a lightsaber.- Peregrin Toker

Re: This one needs an economist or an accountant

Leverage is a killer. See, the mortgages were packaged up and used as collateral in mortgage backed securities and other structured finance products, and there are something like $7-8 trillion MBS products alone plus who knows how many more trillions in structured finance products. The problem as Janet Tavakoli explains in her book, is that the assumptions behind the valuation of those products is full of crap, and the models are all wrong, in short, they assumed good times forever and were never stress tested. Well, now they're getting stressed and as Ms. Tavakoli predicted they're all going kaboom and wiping out trillions of dollars.

In addition to that, all the financials tried to short oil contracts last year and into this year when the price was going up, then they all tried to go long when the price was topping out, and this happened with several other commodities. So they lost huge when they got short-squeezed by the rising price, then got raped again when prices fell. Who knows how many billions got lost there, probably in the hundreds. And of course they took that shit and leveraged it with various derivatives & structured finance products as was done with housing, so you end up with a loss multiplier effect.

In addition to that, all the financials tried to short oil contracts last year and into this year when the price was going up, then they all tried to go long when the price was topping out, and this happened with several other commodities. So they lost huge when they got short-squeezed by the rising price, then got raped again when prices fell. Who knows how many billions got lost there, probably in the hundreds. And of course they took that shit and leveraged it with various derivatives & structured finance products as was done with housing, so you end up with a loss multiplier effect.

Lusankya: Deal!

Say, do you want it to be a threesome with your wife? Or a foursome with your wife and sister-in-law? I'm up for either.

-

Alan Bolte

- Sith Devotee

- Posts: 2611

- Joined: 2002-07-05 12:17am

- Location: Columbus, OH

Re: This one needs an economist or an accountant

I don't think aerius explained that very well for people who don't know terms like 'leverage.' When you borrow money, and use that to purchase an investment product or make a loan, the resulting multiplier effect is called leverage. What multiplier effect? Well, if I invest $1000, and the investment doubles, I now have $2000, for a gain on investment of 100%. If I invest my own $1000, plus $4000 in borrowed money, then I have $5000 invested. If that doubles, then I now have $10000. Subtract the $4000 borrowed, plus interest, and I have a bit less than $6000. Instead of gaining 100% from my investment, I have instead gained nearly 500%, all because I borrowed money. The multiplier effect works in the opposite direction as well: if my unleveraged $1000 investment is cut in half, then I still have $500. If the $1000 investment I leveraged with $4000 of borrowed money is cut in half, then I have $2500 minus the $4000 borrowed, for a total of -1500 (ignoring interest). Boy, I could really use a bailout. That's actually a very conservative amount of leverage by the standards of the banking world. The banks borrow from each other, but they also borrow from you and I: that's what your savings account is.

Also, as aerius mentioned, the banks are also losing money not just on home loans (and finance products based on home loans), but on a variety of investments, such as commodities futures, business loans, auto loans, credit cards, and unregulated, extremely complex bets called derivatives. Commodities futures are a fairly simple, regulated kind of derivative.

Also, as aerius mentioned, the banks are also losing money not just on home loans (and finance products based on home loans), but on a variety of investments, such as commodities futures, business loans, auto loans, credit cards, and unregulated, extremely complex bets called derivatives. Commodities futures are a fairly simple, regulated kind of derivative.

Any job worth doing with a laser is worth doing with many, many lasers. -Khrima

There's just no arguing with some people once they've made their minds up about something, and I accept that. That's why I kill them. -Othar

Avatar credit

There's just no arguing with some people once they've made their minds up about something, and I accept that. That's why I kill them. -Othar

Avatar credit

-

CaptainChewbacca

- Browncoat Wookiee

- Posts: 15746

- Joined: 2003-05-06 02:36am

- Location: Deep beneath Boatmurdered.

Re: This one needs an economist or an accountant

So, the mortgages were used as something like collateral to get loans that were tens of times bigger than the values of the mortgage?

Stuart: The only problem is, I'm losing track of which universe I'm in.

You kinda look like Jesus. With a lightsaber.- Peregrin Toker

You kinda look like Jesus. With a lightsaber.- Peregrin Toker

-

The Duchess of Zeon

- Gözde

- Posts: 14566

- Joined: 2002-09-18 01:06am

- Location: Exiled in the Pale of Settlement.

Re: This one needs an economist or an accountant

CaptainChewbacca wrote:So, the mortgages were used as something like collateral to get loans that were tens of times bigger than the values of the mortgage?

Bingo. That is about as correct as it can be when condensed down to a single sentence.

The threshold for inclusion in Wikipedia is verifiability, not truth. -- Wikipedia's No Original Research policy page.

In 1966 the Soviets find something on the dark side of the Moon. In 2104 they come back. -- Red Banner / White Star, a nBSG continuation story. Updated to Chapter 4.0 -- 14 January 2013.

In 1966 the Soviets find something on the dark side of the Moon. In 2104 they come back. -- Red Banner / White Star, a nBSG continuation story. Updated to Chapter 4.0 -- 14 January 2013.

Re: This one needs an economist or an accountant

Yup. And then the stuff they got by putting up the mortgages as collateral was itself used as collateral for even more crap. Yet another multiplier in there, geometric growth, gotta love it, until things go the wrong way. Then there isn't enough money in the world to even make a dent in the red ink.CaptainChewbacca wrote:So, the mortgages were used as something like collateral to get loans that were tens of times bigger than the values of the mortgage?

Lusankya: Deal!

Say, do you want it to be a threesome with your wife? Or a foursome with your wife and sister-in-law? I'm up for either.

Re: This one needs an economist or an accountant

There's three additional elements to consider.

1) The various programs extend well beyond mortgage-backed securities. For example, the FDIC limit has been increased from $100K to $250K, the Treasury has guaranteed all money market deposits as of Sept. 19, and the Treasury has started backing some short-term commercial paper.

2) It depends on why the assets are written down. If the write down is caused by fundamentals, then there would be a connection between foreclosures and the value of the security, though amplified for the leverage aspect. However, under new accounting standards banks are now required to be more aggressive in marking their assets to market. Essentially, banks now value more assets based on what they could sell them for in the market rather than what they would collect if they held the assets until maturity. Even if your MBS is funded 100% with equity and is composed of people who are insanely creditworthy borrowers, that security is no longer worth par given the absolute chaos that continues persists in fixed income markets. The impact of falling values of securities in the secondary market would also be amplified by leverage. The exact accounting rules are complicated and I can't say what percentage of banks assets fall into mark-to-market categories, but my guess is that it's a meaningful amount.

3) My guess is that the foreclosures number quoted only references residential properties. Commercial mortgage backed securities are also a major market and have suffered as well (and will get worse as consumer spending plummets).

1) The various programs extend well beyond mortgage-backed securities. For example, the FDIC limit has been increased from $100K to $250K, the Treasury has guaranteed all money market deposits as of Sept. 19, and the Treasury has started backing some short-term commercial paper.

2) It depends on why the assets are written down. If the write down is caused by fundamentals, then there would be a connection between foreclosures and the value of the security, though amplified for the leverage aspect. However, under new accounting standards banks are now required to be more aggressive in marking their assets to market. Essentially, banks now value more assets based on what they could sell them for in the market rather than what they would collect if they held the assets until maturity. Even if your MBS is funded 100% with equity and is composed of people who are insanely creditworthy borrowers, that security is no longer worth par given the absolute chaos that continues persists in fixed income markets. The impact of falling values of securities in the secondary market would also be amplified by leverage. The exact accounting rules are complicated and I can't say what percentage of banks assets fall into mark-to-market categories, but my guess is that it's a meaningful amount.

3) My guess is that the foreclosures number quoted only references residential properties. Commercial mortgage backed securities are also a major market and have suffered as well (and will get worse as consumer spending plummets).

"Typical Canadian wimpiness. That's why you have the snowball and we have the H-bomb." Grandpa Simpson

-

Ryan Thunder

- Village Idiot

- Posts: 4139

- Joined: 2007-09-16 07:53pm

- Location: Canada

Re: This one needs an economist or an accountant

Who's brilliant-ass idea was it to let people borrow money with borrowed money?The Duchess of Zeon wrote:Bingo. That is about as correct as it can be when condensed down to a single sentence.CaptainChewbacca wrote:So, the mortgages were used as something like collateral to get loans that were tens of times bigger than the values of the mortgage?

SDN Worlds 5: Sanctum

Re: This one needs an economist or an accountant

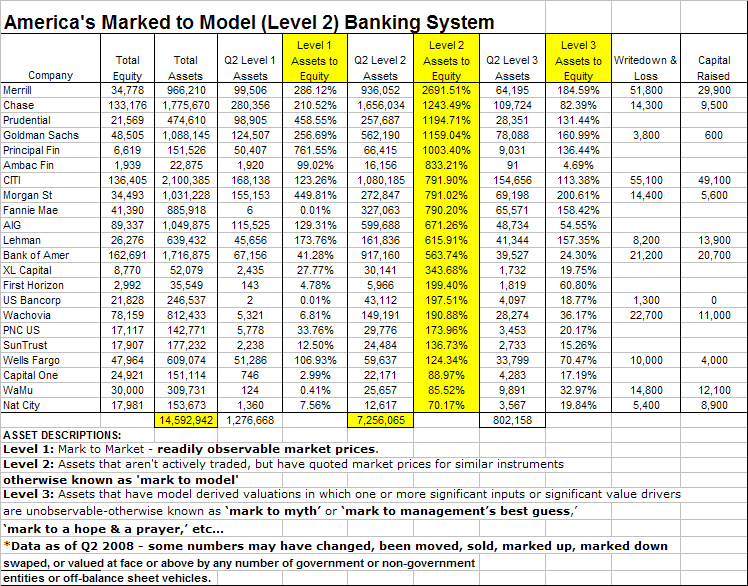

With regards to the second point, this handy chart from Mr. Mortgage provides an answer. Only Level 1 assets are mark to market.

This post is a 100% natural organic product.

The slight variations in spelling and grammar enhance its individual character and beauty and in no way are to be considered flaws or defects

I'm not sure why people choose 'To Love is to Bury' as their wedding song...It's about a murder-suicide

- Margo Timmins

When it becomes serious, you have to lie

- Jean-Claude Juncker

The slight variations in spelling and grammar enhance its individual character and beauty and in no way are to be considered flaws or defects

I'm not sure why people choose 'To Love is to Bury' as their wedding song...It's about a murder-suicide

- Margo Timmins

When it becomes serious, you have to lie

- Jean-Claude Juncker

-

Uraniun235

- Emperor's Hand

- Posts: 13772

- Joined: 2002-09-12 12:47am

- Location: OREGON

- Contact:

Re: This one needs an economist or an accountant

it's called "innovation" or "innovative banking" or some such shit like thatRyan Thunder wrote:Who's brilliant-ass idea was it to let people borrow money with borrowed money?

me, I'd like to see some "innovative justice"

"There is no "taboo" on using nuclear weapons." -Julhelm What is Project Zohar?

What is Project Zohar?

"On a serious note (well not really) I did sometimes jump in and rate nBSG episodes a '5' before the episode even aired or I saw it." - RogueIce explaining that episode ratings on SDN tv show threads are bunk

"On a serious note (well not really) I did sometimes jump in and rate nBSG episodes a '5' before the episode even aired or I saw it." - RogueIce explaining that episode ratings on SDN tv show threads are bunk

-

The Kernel

- Emperor's Hand

- Posts: 7438

- Joined: 2003-09-17 02:31am

- Location: Kweh?!

Re: This one needs an economist or an accountant

If you want a really good overview of why the financial crisis occurred (in five easy steps), read this:

Joseph E. Stiglitz wrote: No. 1: Firing the Chairman

In 1987 the Reagan administration decided to remove Paul Volcker as chairman of the Federal Reserve Board and appoint Alan Greenspan in his place. Volcker had done what central bankers are supposed to do. On his watch, inflation had been brought down from more than 11 percent to under 4 percent. In the world of central banking, that should have earned him a grade of A+++ and assured his re-appointment. But Volcker also understood that financial markets need to be regulated. Reagan wanted someone who did not believe any such thing, and he found him in a devotee of the objectivist philosopher and free-market zealot Ayn Rand.

Greenspan played a double role. The Fed controls the money spigot, and in the early years of this decade, he turned it on full force. But the Fed is also a regulator. If you appoint an anti-regulator as your enforcer, you know what kind of enforcement you’ll get. A flood of liquidity combined with the failed levees of regulation proved disastrous.

Greenspan presided over not one but two financial bubbles. After the high-tech bubble popped, in 2000–2001, he helped inflate the housing bubble. The first responsibility of a central bank should be to maintain the stability of the financial system. If banks lend on the basis of artificially high asset prices, the result can be a meltdown—as we are seeing now, and as Greenspan should have known. He had many of the tools he needed to cope with the situation. To deal with the high-tech bubble, he could have increased margin requirements (the amount of cash people need to put down to buy stock). To deflate the housing bubble, he could have curbed predatory lending to low-income households and prohibited other insidious practices (the no-documentation—or “liar”—loans, the interest-only loans, and so on). This would have gone a long way toward protecting us. If he didn’t have the tools, he could have gone to Congress and asked for them.

Of course, the current problems with our financial system are not solely the result of bad lending. The banks have made mega-bets with one another through complicated instruments such as derivatives, credit-default swaps, and so forth. With these, one party pays another if certain events happen—for instance, if Bear Stearns goes bankrupt, or if the dollar soars. These instruments were originally created to help manage risk—but they can also be used to gamble. Thus, if you felt confident that the dollar was going to fall, you could make a big bet accordingly, and if the dollar indeed fell, your profits would soar. The problem is that, with this complicated intertwining of bets of great magnitude, no one could be sure of the financial position of anyone else—or even of one’s own position. Not surprisingly, the credit markets froze.

Here too Greenspan played a role. When I was chairman of the Council of Economic Advisers, during the Clinton administration, I served on a committee of all the major federal financial regulators, a group that included Greenspan and Treasury Secretary Robert Rubin. Even then, it was clear that derivatives posed a danger. We didn’t put it as memorably as Warren Buffett—who saw derivatives as “financial weapons of mass destruction”—but we took his point. And yet, for all the risk, the deregulators in charge of the financial system—at the Fed, at the Securities and Exchange Commission, and elsewhere—decided to do nothing, worried that any action might interfere with “innovation” in the financial system. But innovation, like “change,” has no inherent value. It can be bad (the “liar” loans are a good example) as well as good.

No. 2: Tearing Down the Walls

The deregulation philosophy would pay unwelcome dividends for years to come. In November 1999, Congress repealed the Glass-Steagall Act—the culmination of a $300 million lobbying effort by the banking and financial-services industries, and spearheaded in Congress by Senator Phil Gramm. Glass-Steagall had long separated commercial banks (which lend money) and investment banks (which organize the sale of bonds and equities); it had been enacted in the aftermath of the Great Depression and was meant to curb the excesses of that era, including grave conflicts of interest. For instance, without separation, if a company whose shares had been issued by an investment bank, with its strong endorsement, got into trouble, wouldn’t its commercial arm, if it had one, feel pressure to lend it money, perhaps unwisely? An ensuing spiral of bad judgment is not hard to foresee. I had opposed repeal of Glass-Steagall. The proponents said, in effect, Trust us: we will create Chinese walls to make sure that the problems of the past do not recur. As an economist, I certainly possessed a healthy degree of trust, trust in the power of economic incentives to bend human behavior toward self-interest—toward short-term self-interest, at any rate, rather than Tocqueville’s “self interest rightly understood.”

The most important consequence of the repeal of Glass-Steagall was indirect—it lay in the way repeal changed an entire culture. Commercial banks are not supposed to be high-risk ventures; they are supposed to manage other people’s money very conservatively. It is with this understanding that the government agrees to pick up the tab should they fail. Investment banks, on the other hand, have traditionally managed rich people’s money—people who can take bigger risks in order to get bigger returns. When repeal of Glass-Steagall brought investment and commercial banks together, the investment-bank culture came out on top. There was a demand for the kind of high returns that could be obtained only through high leverage and big risktaking.

There were other important steps down the deregulatory path. One was the decision in April 2004 by the Securities and Exchange Commission, at a meeting attended by virtually no one and largely overlooked at the time, to allow big investment banks to increase their debt-to-capital ratio (from 12:1 to 30:1, or higher) so that they could buy more mortgage-backed securities, inflating the housing bubble in the process. In agreeing to this measure, the S.E.C. argued for the virtues of self-regulation: the peculiar notion that banks can effectively police themselves. Self-regulation is preposterous, as even Alan Greenspan now concedes, and as a practical matter it can’t, in any case, identify systemic risks—the kinds of risks that arise when, for instance, the models used by each of the banks to manage their portfolios tell all the banks to sell some security all at once.

As we stripped back the old regulations, we did nothing to address the new challenges posed by 21st-century markets. The most important challenge was that posed by derivatives. In 1998 the head of the Commodity Futures Trading Commission, Brooksley Born, had called for such regulation—a concern that took on urgency after the Fed, in that same year, engineered the bailout of Long-Term Capital Management, a hedge fund whose trillion-dollar-plus failure threatened global financial markets. But Secretary of the Treasury Robert Rubin, his deputy, Larry Summers, and Greenspan were adamant—and successful—in their opposition. Nothing was done.

No. 3: Applying the Leeches

Then along came the Bush tax cuts, enacted first on June 7, 2001, with a follow-on installment two years later. The president and his advisers seemed to believe that tax cuts, especially for upper-income Americans and corporations, were a cure-all for any economic disease—the modern-day equivalent of leeches. The tax cuts played a pivotal role in shaping the background conditions of the current crisis. Because they did very little to stimulate the economy, real stimulation was left to the Fed, which took up the task with unprecedented low-interest rates and liquidity. The war in Iraq made matters worse, because it led to soaring oil prices. With America so dependent on oil imports, we had to spend several hundred billion more to purchase oil—money that otherwise would have been spent on American goods. Normally this would have led to an economic slowdown, as it had in the 1970s. But the Fed met the challenge in the most myopic way imaginable. The flood of liquidity made money readily available in mortgage markets, even to those who would normally not be able to borrow. And, yes, this succeeded in forestalling an economic downturn; America’s household saving rate plummeted to zero. But it should have been clear that we were living on borrowed money and borrowed time.

The cut in the tax rate on capital gains contributed to the crisis in another way. It was a decision that turned on values: those who speculated (read: gambled) and won were taxed more lightly than wage earners who simply worked hard. But more than that, the decision encouraged leveraging, because interest was tax-deductible. If, for instance, you borrowed a million to buy a home or took a $100,000 home-equity loan to buy stock, the interest would be fully deductible every year. Any capital gains you made were taxed lightly—and at some possibly remote day in the future. The Bush administration was providing an open invitation to excessive borrowing and lending—not that American consumers needed any more encouragement.

No. 4: Faking the Numbers

Meanwhile, on July 30, 2002, in the wake of a series of major scandals—notably the collapse of WorldCom and Enron—Congress passed the Sarbanes-Oxley Act. The scandals had involved every major American accounting firm, most of our banks, and some of our premier companies, and made it clear that we had serious problems with our accounting system. Accounting is a sleep-inducing topic for most people, but if you can’t have faith in a company’s numbers, then you can’t have faith in anything about a company at all. Unfortunately, in the negotiations over what became Sarbanes-Oxley a decision was made not to deal with what many, including the respected former head of the S.E.C. Arthur Levitt, believed to be a fundamental underlying problem: stock options. Stock options have been defended as providing healthy incentives toward good management, but in fact they are “incentive pay” in name only. If a company does well, the C.E.O. gets great rewards in the form of stock options; if a company does poorly, the compensation is almost as substantial but is bestowed in other ways. This is bad enough. But a collateral problem with stock options is that they provide incentives for bad accounting: top management has every incentive to provide distorted information in order to pump up share prices.

The incentive structure of the rating agencies also proved perverse. Agencies such as Moody’s and Standard & Poor’s are paid by the very people they are supposed to grade. As a result, they’ve had every reason to give companies high ratings, in a financial version of what college professors know as grade inflation. The rating agencies, like the investment banks that were paying them, believed in financial alchemy—that F-rated toxic mortgages could be converted into products that were safe enough to be held by commercial banks and pension funds. We had seen this same failure of the rating agencies during the East Asia crisis of the 1990s: high ratings facilitated a rush of money into the region, and then a sudden reversal in the ratings brought devastation. But the financial overseers paid no attention.

No. 5: Letting It Bleed

The final turning point came with the passage of a bailout package on October 3, 2008—that is, with the administration’s response to the crisis itself. We will be feeling the consequences for years to come. Both the administration and the Fed had long been driven by wishful thinking, hoping that the bad news was just a blip, and that a return to growth was just around the corner. As America’s banks faced collapse, the administration veered from one course of action to another. Some institutions (Bear Stearns, A.I.G., Fannie Mae, Freddie Mac) were bailed out. Lehman Brothers was not. Some shareholders got something back. Others did not.

The original proposal by Treasury Secretary Henry Paulson, a three-page document that would have provided $700 billion for the secretary to spend at his sole discretion, without oversight or judicial review, was an act of extraordinary arrogance. He sold the program as necessary to restore confidence. But it didn’t address the underlying reasons for the loss of confidence. The banks had made too many bad loans. There were big holes in their balance sheets. No one knew what was truth and what was fiction. The bailout package was like a massive transfusion to a patient suffering from internal bleeding—and nothing was being done about the source of the problem, namely all those foreclosures. Valuable time was wasted as Paulson pushed his own plan, “cash for trash,” buying up the bad assets and putting the risk onto American taxpayers. When he finally abandoned it, providing banks with money they needed, he did it in a way that not only cheated America’s taxpayers but failed to ensure that the banks would use the money to re-start lending. He even allowed the banks to pour out money to their shareholders as taxpayers were pouring money into the banks.

The other problem not addressed involved the looming weaknesses in the economy. The economy had been sustained by excessive borrowing. That game was up. As consumption contracted, exports kept the economy going, but with the dollar strengthening and Europe and the rest of the world declining, it was hard to see how that could continue. Meanwhile, states faced massive drop-offs in revenues—they would have to cut back on expenditures. Without quick action by government, the economy faced a downturn. And even if banks had lent wisely—which they hadn’t—the downturn was sure to mean an increase in bad debts, further weakening the struggling financial sector.

The administration talked about confidence building, but what it delivered was actually a confidence trick. If the administration had really wanted to restore confidence in the financial system, it would have begun by addressing the underlying problems—the flawed incentive structures and the inadequate regulatory system.

Was there any single decision which, had it been reversed, would have changed the course of history? Every decision—including decisions not to do something, as many of our bad economic decisions have been—is a consequence of prior decisions, an interlinked web stretching from the distant past into the future. You’ll hear some on the right point to certain actions by the government itself—such as the Community Reinvestment Act, which requires banks to make mortgage money available in low-income neighborhoods. (Defaults on C.R.A. lending were actually much lower than on other lending.) There has been much finger-pointing at Fannie Mae and Freddie Mac, the two huge mortgage lenders, which were originally government-owned. But in fact they came late to the subprime game, and their problem was similar to that of the private sector: their C.E.O.’s had the same perverse incentive to indulge in gambling.

The truth is most of the individual mistakes boil down to just one: a belief that markets are self-adjusting and that the role of government should be minimal. Looking back at that belief during hearings this fall on Capitol Hill, Alan Greenspan said out loud, “I have found a flaw.” Congressman Henry Waxman pushed him, responding, “In other words, you found that your view of the world, your ideology, was not right; it was not working.” “Absolutely, precisely,” Greenspan said. The embrace by America—and much of the rest of the world—of this flawed economic philosophy made it inevitable that we would eventually arrive at the place we are today.

Re: This one needs an economist or an accountant

I've got a good one also:

link to $50 Billion dollar Ponzi scheme

Key stuff bolded:

Still, all but admitting that the entire company was a Ponzi scheme, he has lost fifty billion dollars, and his 'peers' consider him a person of integrity. Between this and the Auto Industry Bailout that got canceled, tomorrow should be interesting.

link to $50 Billion dollar Ponzi scheme

Key stuff bolded:

Article was bigger than I thought.David Glovin and David Scheer wrote: Dec. 11 (Bloomberg) -- Bernard Madoff, founder and president of a New York firm that invested funds for wealthy individuals, hedge funds and other institutions, was charged with operating what he told employees was a long-running $50 billion Ponzi scheme in what may be one of the largest frauds in history.

Madoff, 70, head of Bernard L. Madoff Investment Securities LLC, was arrested today at 8:30 a.m. by the FBI and appeared before U.S. Magistrate Judge Douglas Eaton in Manhattan federal court. Charged in a criminal complaint with a single count of securities fraud, he was released on $10 million bond guaranteed by his wife and secured by his apartment. Madoff, wearing a white-striped shirt, dark-colored pants and no tie, looked down as he left the courtroom with his wife, declining to comment.

“It’s all just one big lie,” Madoff told his employees on Dec. 10, according to the government. The firm, Madoff allegedly said to them, is “basically, a giant Ponzi scheme.”

Madoff faces as much as 20 years in prison and a $5 million fine if convicted. His New York-based firm was the 23rd largest market maker on Nasdaq in October, handling a daily average of about 50 million shares a day, exchange data show. It specialized in handling orders from online brokers in some of the largest U.S. companies, including General Electric Co. and Citigroup Inc.

‘One of The Pioneers’

“He’s one of the pioneers of modern Wall Street,” said James Angel, an associate business professor at Georgetown University in Washington. Madoff’s firm was among the first to automate market-making, in which a dealer continually buys and sells stock. The company was among the largest to offer “payment for order flow,” or paying to handle customer orders.

“The exchanges didn’t like the practice and questioned whether customers got the best price,” Angel said.

Madoff was also sued today by the U.S. Securities and Exchange Commission.

“Bernard Madoff is a longstanding leader in the financial services industry,” said defense lawyer Dan Horwitz. “We will fight to get through this unfortunate set of events. He’s a person of integrity.”

Fix Asset Management in New York, which had at least $400 million with Madoff, said it was checking with its lawyers regarding its holdings.

“We are very shocked,” John Fix, the son of founder Charles Fix, said by telephone from Greece. “We put in redemptions in the past few months and got our money back no problem. We are just so surprised about all this.”

‘Accelerating Their Redemptions’

Thomas Ajamie, a securities lawyer in Houston who won a $429 million arbitration award against Paine Webber Group in 2001, speculated that Madoff “couldn’t keep the Ponzi scheme going because investors were accelerating their redemptions.”

New York-based Fairfield Greenwich Group runs the $7.3 billion Fairfield Sentry Ltd., a fund that invested in Madoff. Andrew Ludwig, a spokesman for Fairfield, declined to immediately comment.

The SEC in its complaint, also filed in Manhattan federal court, accused Madoff of a “multi-billion dollar Ponzi scheme that he perpetrated on advisory clients of his firm.”

The agency said it’s seeking emergency relief for investors, including an asset freeze and the appointment of a receiver for the firm. Ira Sorkin, another defense lawyer for Madoff, couldn’t be immediately reached for comment.

Advisory Business

Madoff ran his investment advisory business from a separate floor of his firm’s office, keeping financial statements “under lock and key,” prosecutors said. Early in December, he told one employee that clients wanted to redeem about $7 billion and that he was struggling to free up the funds, the government said. After he told another staff member Dec. 9 that he wanted to pay annual bonuses before the year’s end, two months early, a pair of senior employees asked to speak with him, prosecutors said.

They had noticed he had been suffering from a “great deal of stress” and wanted to know what was happening, the U.S. said. When one of them challenged his explanations, Madoff invited them to his Manhattan apartment, saying he “wasn’t sure he would be able to hold it together” if they continued talking at the office, the government said.

While meeting the pair at his home yesterday, Madoff conceded that he was “finished,” that his advisory business is “all just one big lie” and “basically, a giant Ponzi scheme,” the government said. The business had been insolvent for years with losses of about $50 billion, he told the employees, according to the criminal and SEC complaints.

Madoff said he had about $200 million to $300 million left and planned to distribute money to select employees, family and friends before surrendering to authorities in about a week, the government said.

Confessed to FBI

Madoff allegedly confessed to FBI agent Theodore Cacioppi on Dec. 11, saying there was “no innocent explanation,” the SEC said in its complaint. Madoff said it was his fault and he had “paid investors with money that wasn’t there.” He also said he was “insolvent” and he expected to go to jail, it said.

The Madoff firm had about $17.1 billion in assets under management as of Nov. 17, according to NASD records. At least 50 percent of its clients were hedge funds, and others included banks and wealthy individuals, according to the records.

Madoff started his firm in 1960 with $5,000 of savings and took advantage of securities-law changes in the 1970s designed to spur competition in U.S. stock markets, according to a profile posted on the Web site Finance Tech.

75 Percent Owner

Madoff, who owned more than 75 percent of his firm, and his brother Peter are the only two individuals listed on regulatory records as “direct owners and executive officers.”

Peter Madoff was a board member of the St. Louis brokerage firm A.G. Edwards Inc. from 2001 through last year, when it was sold to Wachovia Corp.

Bernard Madoff served as vice chairman of the National Association of Securities Dealers, a member of its board of governors, and chairman of its New York region, according to the SEC Web site. He was also a member of Nasdaq Stock Market’s board of governors and its executive committee and served as chairman of its trading committee.

He was chief of the Securities Industry Association’s trading committee in the 1990s and earlier this decade, where he represented brokerage firms in discussions with regulators about new stock-market rules as electronic-trading systems and networks gained prominence.

He was an early advocate for electronic trading, participating in roundtable discussions at the SEC as regulators weighed trading stocks in penny increments. His firm was among the first to make markets in New York Stock Exchange listed stocks outside of the Big Board, relying instead on Nasdaq.

‘Third Market Makers’

“These guys were one of the original, if not the original, third market makers,” said Joseph Saluzzi, the co-head of equity trading at Themis Trading LLC in Chatham, New Jersey. “They had a great business and they were good with their clients. They were around for a long time. He’s a well-respected guy in the industry.”

At 6:30 p.m., security guards at the front desk of the lipstick-shaped building on Third Avenue in midtown Manhattan housing Madoff’s office were turning people away. Ganesh Sewpershad, a messenger with Speeddox, said he had been trying to deliver mail for 20 minutes and was told to return tomorrow.

Madoff’s Web site advertises the “high ethical standards” of his firm.

“In an era of faceless organizations owned by other equally faceless organizations, Bernard L. Madoff Investment Securities LLC harks back to an earlier era in the financial world: The owner’s name is on the door,” according to the Web site. “Clients know that Bernard Madoff has a personal interest in maintaining the unblemished record of value, fair-dealing, and high ethical standards that has always been the firm’s hallmark.”

The case is U.S. v. Madoff, 08-MAG-02735, U.S. District Court for the Southern District of New York (Manhattan)

Still, all but admitting that the entire company was a Ponzi scheme, he has lost fifty billion dollars, and his 'peers' consider him a person of integrity. Between this and the Auto Industry Bailout that got canceled, tomorrow should be interesting.

-

K. A. Pital

- Glamorous Commie

- Posts: 20813

- Joined: 2003-02-26 11:39am

- Location: Elysium

Re: This one needs an economist or an accountant

50 billion scam, and his "peers" say he's a honest person who wanted financial business to flourish!  You can't make that shit up.

You can't make that shit up.

Now the US gets some taste of those Ponzi schemes which were used by oligarchs to get rich in Russia. I remember how people rolled eyes when facts of universal hatred of "honest buzinesmans" aka the oligarchs in Russia were presented: of course they are "honest" people and not scammers who blew the people for billions.

"High ethical standards" of a person in the financial sphere today sounds like a strong enough joke to cause a few laughs just when spoken aloud, much more laughs when spoken earnestly by a financial mobster!

Now the US gets some taste of those Ponzi schemes which were used by oligarchs to get rich in Russia. I remember how people rolled eyes when facts of universal hatred of "honest buzinesmans" aka the oligarchs in Russia were presented: of course they are "honest" people and not scammers who blew the people for billions.

"High ethical standards" of a person in the financial sphere today sounds like a strong enough joke to cause a few laughs just when spoken aloud, much more laughs when spoken earnestly by a financial mobster!

Lì ci sono chiese, macerie, moschee e questure, lì frontiere, prezzi inaccessibile e freddure

Lì paludi, minacce, cecchini coi fucili, documenti, file notturne e clandestini

Qui incontri, lotte, passi sincronizzati, colori, capannelli non autorizzati,

Uccelli migratori, reti, informazioni, piazze di Tutti i like pazze di passioni...

...La tranquillità è importante ma la libertà è tutto!

Lì paludi, minacce, cecchini coi fucili, documenti, file notturne e clandestini

Qui incontri, lotte, passi sincronizzati, colori, capannelli non autorizzati,

Uccelli migratori, reti, informazioni, piazze di Tutti i like pazze di passioni...

...La tranquillità è importante ma la libertà è tutto!

Assalti Frontali